- Why Testing Methodology Matters More Than Strategy Design

- The Core Problem: Strategy Failure Is Usually a Testing Failure

- Backtesting: Controlled Simulation of Historical Reality

- What Backtesting Can Show (and What It Cannot)

- The Overfitting Trap: The Silent Backtesting Risk

- Forward Testing: Exposure to Reality, Not History

- Why Forward Testing Matters More in Crypto Than Traditional Markets

- Where Each Testing Method Fits in the Strategy Lifecycle

- The False Confidence Problem

- Backtesting vs Forward Testing Is Not a Choice

- A Modern Testing Mindset (2025)

- Why This Matters for Investors, Not Just Traders

- Core Crypto Indicators Explained

- How Professionals Actually Use Them in 2025

- Relative Strength Index (RSI): Measuring Momentum, Not Value

- What RSI Is Commonly Used For

- What RSI Is Not Designed to Do

- Moving Averages (SMA & EMA): Defining Market Structure

- Professional Use Cases

- MACD: Momentum Changes Within Trends

- Bollinger Bands: Volatility Awareness, Not Direction

- Average True Range (ATR): Risk Measurement, Not Signal Generation

- Core Crypto Indicators and Their Primary Function (2025)

- Why No Single Indicator Works Alone

- Common Indicator Misuse vs Professional Interpretation

- How Indicators Connect to Portfolio-Level Decisions

- Building a Robust Testing Framework: From Validation to Deployment (2025 Perspective)

- The Transition Problem: Why Most Strategies Fail Between Testing and Deployment

- A Professional Testing Stack (Sequential, Not Simultaneous)

- Why Portfolio Context Changes Everything

- When Backtesting and Forward Testing Disagree

- Behavioral Risk: The Invisible Variable

- The Role of AI and Modern Tooling (2025 Reality)

- What a Complete Testing Framework Actually Achieves

- Testing Is a Risk Discipline, Not a Performance Tool

- Disclaimer

Crypto strategies fail far more often because of how they are tested than because of the ideas behind them. In today’s fast-moving crypto markets, relying on backtesting alone creates false confidence, while skipping forward testing leaves critical execution risks unseen. Understanding when and why to use each method is essential for building strategies that survive real market conditions, not just historical simulations.

Why Testing Methodology Matters More Than Strategy Design

In 2025, the crypto market no longer suffers from a lack of tools or data. Instead, the biggest source of failure for both retail and professional investors comes from how strategies are tested, not which strategy is chosen.

Backtesting and forward testing are often treated as interchangeable validation steps. In reality, they answer different questions, operate under different assumptions, and expose different types of risk. Misunderstanding this distinction is one of the main reasons strategies that look excellent on paper fail once capital is deployed.

This guide does not frame backtesting and forward testing as competitors. Instead, it explains why neither is sufficient alone, how they complement each other, and how modern market structure in crypto has changed the role of both.

The Core Problem: Strategy Failure Is Usually a Testing Failure

Most strategies that fail in live markets do not fail because:

-

the logic was flawed

-

the indicators were incorrect

-

the asset selection was poor

They fail because:

-

historical assumptions do not hold in live execution

-

market regimes change faster than expected

-

friction costs are underestimated

-

behavioral responses are ignored

Backtesting and forward testing exist to surface different layers of these risks.

Understanding when to use each is not optional — it is foundational.

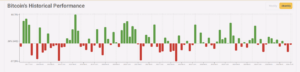

Bitcoin’s monthly historical performance. The sequence of strong gains and deep losses shows how quickly crypto market regimes can shift, which makes naive reliance on past performance dangerous. Source: Forvest.io.

Backtesting: Controlled Simulation of Historical Reality

Backtesting applies a predefined strategy to historical market data to measure how it would have performed under past conditions.

Its primary role is hypothesis validation, not performance confirmation.

In modern crypto analysis, backtesting answers questions such as:

-

Does this logic behave consistently across market cycles?

-

How sensitive is performance to parameter changes?

-

Does the strategy survive high-volatility periods?

-

Are drawdowns structurally acceptable?

Backtesting is powerful precisely because it is fast and repeatable. In minutes, an analyst can simulate years of price action, compare variations, and eliminate weak ideas early.

However, this speed comes with critical limitations.

What Backtesting Can Show (and What It Cannot)

Backtesting is effective at identifying:

-

logical inconsistencies

-

structural weaknesses

-

over-complex strategies

-

unstable parameter dependencies

It is not designed to confirm:

-

execution quality

-

slippage behavior

-

order latency effects

-

psychological pressure

-

live liquidity constraints

In crypto markets especially, historical data often reflects idealized conditions:

-

perfect fills

-

uniform liquidity

-

static fee structures

-

absence of sudden regime shifts

This gap between simulated execution and live reality is where many strategies collapse.

The Overfitting Trap: The Silent Backtesting Risk

One of the most dangerous backtesting pitfalls is overfitting — designing a strategy that performs exceptionally well on past data but poorly on unseen conditions.

Overfitting often appears in subtle forms:

-

excessive parameter tuning

-

curve-fitting to specific volatility regimes

-

optimizing for peak returns instead of robustness

-

ignoring out-of-sample validation

In 2025, this risk is amplified by:

-

AI-assisted optimization tools

-

increased parameter complexity

-

access to massive historical datasets

The more freedom a model has, the easier it becomes to mistake historical coincidence for edge.

Backtesting must therefore be treated as a filter, not a green light.

Forward Testing: Exposure to Reality, Not History

Forward testing — often referred to as paper trading or live simulation — runs a strategy in real-time market conditions without (or with minimal) capital at risk.

Its purpose is fundamentally different from backtesting.

Forward testing answers questions such as:

-

Does execution behave as expected?

-

How large is real slippage relative to assumptions?

-

Do signals arrive too late in fast markets?

-

Does the strategy survive real volatility clusters?

-

Can the process be followed consistently?

Unlike backtesting, forward testing cannot be rushed.

It requires time, discipline, and environmental exposure.

This is precisely why it is valuable.

Why Forward Testing Matters More in Crypto Than Traditional Markets

Crypto markets differ structurally from traditional markets in ways that make forward testing essential:

-

Liquidity can disappear abruptly

-

Volatility clusters are more extreme

-

Market structure evolves rapidly

-

News-driven moves override technical behavior

-

Exchange execution quality varies widely

A strategy that survives backtesting but fails forward testing is not unlucky — it is incomplete.

Forward testing reveals risks that historical data simply cannot model.

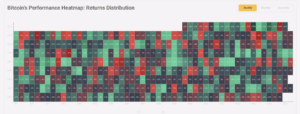

Bitcoin’s weekly performance heatmap (2017–2025). The clustered returns highlight how crypto volatility is regime-based, which forward testing must capture under real market conditions. Source: Forvest.io.

Where Each Testing Method Fits in the Strategy Lifecycle

| Strategy Development Stage | Backtesting Role | Forward Testing Role |

|---|---|---|

| Idea validation | Primary tool | Not suitable |

| Parameter sensitivity | Strong | Limited |

| Regime robustness | Partial | Strong |

| Execution realism | Weak | Critical |

| Behavioral discipline | None | High |

| Capital readiness | Insufficient alone | Essential |

Source: Investopedia, CFA Institute, Forvest Research (2025)

This distinction explains why neither method replaces the other — they operate at different layers of risk.

The False Confidence Problem

A common psychological mistake is assuming that strong backtest performance implies readiness for deployment.

This leads to:

-

premature capital allocation

-

inflated position sizes

-

underestimation of drawdown tolerance

-

emotional breakdown during live losses

Forward testing acts as a reality calibration layer.

It forces the strategist to confront:

-

imperfect fills

-

missed entries

-

delayed exits

-

real-time uncertainty

Many strategies are abandoned during forward testing — not because they are unprofitable, but because they are untradable in practice.

That distinction matters.

Backtesting vs Forward Testing Is Not a Choice

The core mistake is treating this as an either/or decision.

-

Backtesting without forward testing leads to false confidence and fragile strategies

-

Forward testing without backtesting leads to wasted time and unclear expectations

Professional workflows use both — in sequence, with different evaluation criteria.

A Modern Testing Mindset (2025)

In 2025, robust strategy development follows a layered validation approach:

-

Backtesting to validate logic and eliminate weak ideas

-

Out-of-sample testing to reduce overfitting

-

Forward testing to expose execution and behavioral risk

-

Gradual capital deployment with strict risk limits

Each stage answers a different question.

Skipping any step increases the probability of failure — not immediately, but inevitably.

Why This Matters for Investors, Not Just Traders

This framework applies beyond short-term trading systems.

Long-term investors, portfolio allocators, and discretionary decision-makers benefit from:

-

understanding how assumptions behave over time

-

recognizing regime dependency

-

testing allocation logic under live conditions

Testing methodology is not about prediction.

It is about risk containment.

Core Crypto Indicators Explained

How Professionals Actually Use Them in 2025

In 2025, the most effective crypto investors no longer use indicators to chase entries or generate mechanical buy/sell signals. Instead, indicators are applied as contextual analysis tools — frameworks that help interpret market conditions, manage exposure, and reduce behavioral errors.

This section explains the most widely used crypto indicators, not from a textbook perspective, but from how they are actually used by professionals. The focus is on what each indicator measures, what problem it is designed to solve, and where it is most often misunderstood.

The goal remains clarity — not complexity.

Relative Strength Index (RSI): Measuring Momentum, Not Value

The Relative Strength Index (RSI) remains one of the most referenced indicators in crypto markets. Its popularity, however, has also made it one of the most misused.

RSI measures momentum — the speed and persistence of recent price movements — by comparing average gains to average losses over a defined period. It expresses this relationship on a scale from 0 to 100.

RSI momentum behavior on Bitcoin price action. Source: CoinMarketCap

What RSI Is Commonly Used For

-

Identifying momentum strength or weakness

-

Detecting bullish or bearish divergence

-

Understanding momentum regimes (bull vs bear behavior)

-

Comparing relative strength across assets

What RSI Is Not Designed to Do

-

Predict precise reversals

-

Signal exact tops or bottoms

-

Define “cheap” or “expensive” prices

-

Replace trend or volatility analysis

In strong crypto trends, RSI can remain above 60–70 (or below 40–30) for extended periods. Treating “overbought” as an automatic sell signal is one of the most common beginner mistakes.

Professionals interpret RSI in context, focusing on:

-

RSI range behavior across regimes

-

Divergence relative to price structure

-

Multi-timeframe confirmation

RSI becomes most powerful when it is aligned with trend structure, not used against it.

Moving Averages (SMA & EMA): Defining Market Structure

Moving averages are foundational tools across all financial markets. Their purpose is not prediction, but trend definition and noise reduction.

There are two primary types:

-

Simple Moving Average (SMA): Equal weight to all periods

-

Exponential Moving Average (EMA): Greater weight on recent data

Moving averages are inherently lagging — and that is a feature, not a flaw.

Professional Use Cases

-

Identifying dominant trend direction

-

Defining dynamic support and resistance

-

Filtering trades in the direction of the trend

-

Measuring trend strength and persistence

In crypto, where trends are often driven by liquidity cycles and narratives, moving averages help investors avoid fighting the market.

Professionals rarely rely on a single average. Instead, they analyze:

-

Short-term vs long-term averages

-

Slope and distance from price

-

Interaction with broader market structure

Moving averages are not timing tools — they are alignment tools.

MACD: Momentum Changes Within Trends

The Moving Average Convergence Divergence (MACD) combines elements of both trend and momentum. It is derived from the relationship between two EMAs and a signal line.

MACD is most useful for:

-

Identifying momentum shifts within established trends

-

Confirming trend continuation or weakening

-

Detecting divergence between price and momentum

Because MACD is based on moving averages, it is also lagging — especially on higher timeframes. Professionals therefore treat it as a confirmation indicator, not a trigger.

Key professional interpretations include:

-

Histogram expansion vs contraction

-

Momentum changes relative to price structure

-

Alignment with higher-timeframe trends

MACD is most effective when used alongside moving averages, not independently.

Bollinger Bands: Volatility Awareness, Not Direction

Bollinger Bands measure volatility by plotting price relative to a moving average with upper and lower bands based on standard deviation.

They answer one primary question:

Is volatility expanding or compressing?

They do not indicate direction.

Professional use cases include:

-

Identifying volatility contraction before expansion

-

Assessing whether price movement is statistically extreme

-

Adjusting position size during high-volatility regimes

A common misconception is that touching a band implies reversal. In strong trends, price can “walk the band” for extended periods.

Bollinger Bands are best viewed as volatility context tools, not reversal signals.

Average True Range (ATR): Risk Measurement, Not Signal Generation

ATR measures average price movement over a given period. It does not indicate direction, trend, or momentum.

ATR exists almost entirely for risk management.

Professionals use ATR to:

-

Size positions relative to volatility

-

Set stop distances based on market conditions

-

Compare volatility across assets

-

Reduce exposure during unstable regimes

In crypto markets — where volatility regimes shift quickly — ATR is one of the most underrated tools.

Ignoring volatility while focusing only on signals is one of the fastest paths to drawdowns.

Core Crypto Indicators and Their Primary Function (2025)

| Indicator | Category | What It Measures | Primary Professional Use |

|---|---|---|---|

| RSI | Momentum | Speed & strength of price movement | Momentum regime & divergence |

| SMA / EMA | Trend | Directional bias | Trend alignment & filtering |

| MACD | Trend + Momentum | Momentum within trend | Trend confirmation |

| Bollinger Bands | Volatility | Price dispersion | Volatility expansion/compression |

| ATR | Volatility | Average price movement | Risk & position sizing |

Source: Investopedia, TradingView Indicators Library, Forvest Research (2025)

Why No Single Indicator Works Alone

Crypto markets are multi-dimensional systems where price, volume, volatility, liquidity, and sentiment interact simultaneously.

Expecting a single indicator to capture all of this information is unrealistic.

Professional analysis relies on indicator confluence, where each tool answers a different question:

-

Is the market trending? → Moving averages

-

Is momentum supporting it? → RSI / MACD

-

Is volatility stable or expanding? → Bollinger Bands / ATR

-

Is risk acceptable? → Volatility-adjusted sizing

The strength of analysis comes from confluence, not indicator count.

Common Indicator Misuse vs Professional Interpretation

| Indicator | Common Beginner Mistake | Professional Interpretation |

|---|---|---|

| RSI | Selling because RSI > 70 | Evaluate momentum regime & divergence |

| Moving Averages | Trading every crossover | Confirm broader trend first |

| MACD | Trading every signal cross | Use for momentum confirmation |

| Bollinger Bands | Expecting reversal at bands | Assess volatility behavior |

| ATR | Ignoring it completely | Use for sizing & risk control |

Source: CFA Institute, Behavioral Finance Studies, Forvest Research (2025)

How Indicators Connect to Portfolio-Level Decisions

In 2025, indicators are increasingly applied at the portfolio level, not just per asset.

Examples include:

-

Reducing overall exposure during high-volatility regimes

-

Comparing RSI across assets for relative strength

-

Adjusting allocations based on trend regimes

-

Monitoring correlation risk during stress periods

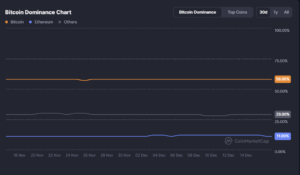

Bitcoin dominance trend highlighting portfolio-level capital rotation across crypto assets. Source: CoinMarketCap

This approach aligns indicators with risk management and allocation logic, rather than speculation.

For readers who want to integrate indicator interpretation with portfolio-level clarity, Forvest tools are built around this philosophy:

Building a Robust Testing Framework: From Validation to Deployment (2025 Perspective)

By the time a strategy reaches this stage, the core logic has already been tested historically and exposed to live conditions. What separates fragile strategies from durable ones in 2025 is not performance optimization, but process design. Professional investors do not ask whether a strategy “works”; they ask under what conditions it fails, how fast it degrades, and how risk is contained when assumptions break.

This section focuses on how backtesting and forward testing are integrated into a single, repeatable framework that supports long-term decision-making rather than short-term performance chasing.

The Transition Problem: Why Most Strategies Fail Between Testing and Deployment

The most common failure point is not idea generation, but transition.

Many strategies look statistically sound in backtests and even survive limited forward testing — yet still fail once real capital is deployed. This usually happens because the testing process answers isolated questions, not systemic ones.

Typical transition failures include:

-

Increasing position size too quickly after early success

-

Ignoring regime changes that invalidate historical assumptions

-

Treating early forward-test results as confirmation instead of sampling

-

Failing to account for correlation and portfolio-level risk

-

Assuming execution quality remains stable under scale

In 2025 crypto markets, where liquidity, volatility, and sentiment can shift rapidly, deployment discipline matters more than entry precision.

A Professional Testing Stack (Sequential, Not Simultaneous)

Robust testing follows a layered structure. Each layer exists to invalidate assumptions, not to confirm beliefs.

Layer 1 — Backtesting (Logic Validation)

Purpose:

-

Verify internal consistency

-

Identify structural weaknesses

-

Eliminate non-robust ideas early

Key questions answered:

-

Does this logic survive different market cycles?

-

Is performance stable across parameter ranges?

-

Are drawdowns structurally acceptable?

Backtesting success only earns permission to continue — nothing more.

Layer 2 — Out-of-Sample & Walk-Forward Testing (Robustness Check)

Purpose:

-

Reduce overfitting

-

Test adaptability across unseen data

Key questions answered:

-

Does performance degrade gracefully outside the optimization window?

-

Is the strategy regime-dependent?

-

Are results statistically repeatable?

This layer filters out strategies that are overly dependent on historical coincidence.

Layer 3 — Forward Testing (Execution & Behavior Exposure)

Purpose:

-

Validate execution realism

-

Expose behavioral and operational risk

Key questions answered:

-

Are fills and slippage within expectations?

-

Can the strategy be executed consistently in real time?

-

Does volatility alter behavior or discipline?

Forward testing is not about profitability — it is about survivability under live conditions.

Layer 4 — Graduated Capital Deployment (Risk Containment)

Purpose:

-

Observe strategy behavior under real financial pressure

-

Limit damage during inevitable assumption failures

Key principles:

-

Start with minimal exposure

-

Increase size slowly, based on process stability — not returns

-

Monitor deviation from expected behavior, not short-term P/L

This layer protects capital while exposing remaining blind spots.

Why Portfolio Context Changes Everything

Most retail testing frameworks evaluate strategies in isolation. Professional frameworks do not.

In real portfolios:

-

Assets interact

-

Correlations change

-

Volatility clusters amplify risk

-

Drawdowns compound psychologically

A strategy that performs well alone may destabilize a portfolio when combined with others.

By 2025, serious investors increasingly test strategies at the portfolio level, evaluating:

-

Correlation impact

-

Volatility contribution

-

Drawdown clustering

-

Regime sensitivity across assets

This is where testing moves beyond “strategy performance” into risk architecture.

When Backtesting and Forward Testing Disagree

Disagreement between historical and live results is not a failure — it is information.

Common causes include:

-

Liquidity regime shifts

-

Structural market changes

-

Execution friction underestimated in backtests

-

Behavioral bias under real-time pressure

Professional response is not to force alignment, but to:

-

Reduce exposure

-

Reassess assumptions

-

Adjust expectations

-

Pause deployment if necessary

The goal is capital preservation, not intellectual validation.

Behavioral Risk: The Invisible Variable

No testing framework is complete without acknowledging behavior.

Strategies fail not only because markets change, but because people react poorly to uncertainty.

Common behavioral breakdowns include:

-

Abandoning strategies after statistically normal drawdowns

-

Overreacting to short-term variance

-

Adjusting rules mid-test

-

Increasing size after wins

-

Seeking confirmation instead of evidence

Forward testing exists largely to expose these behaviors before they become expensive.

Testing is not only about the strategy — it is about the strategist.

The Role of AI and Modern Tooling (2025 Reality)

AI does not replace backtesting or forward testing. It enhances interpretation.

In modern crypto analysis, AI-assisted systems help:

-

Detect abnormal deviations from historical patterns

-

Identify regime shifts earlier

-

Monitor execution drift

-

Aggregate multi-strategy risk exposure

-

Reduce cognitive bias in evaluation

The value of AI lies in contextual awareness, not signal generation.

This aligns with Forvest’s philosophy:

Indicators, testing, and AI are used to manage risk, not to predict price.

What a Complete Testing Framework Actually Achieves

A mature testing process does not aim to find perfect strategies.

It aims to:

-

Eliminate fragile ideas early

-

Surface hidden risks

-

Align expectations with reality

-

Reduce emotional decision-making

-

Protect capital during uncertainty

Strategies that survive this process are not guaranteed to outperform — but they are far less likely to fail catastrophically.

Testing Is a Risk Discipline, Not a Performance Tool

Backtesting and forward testing are not competing methods. They are complementary layers of a single risk-management system.

Backtesting answers:

“Does this idea make sense historically?”

Forward testing answers:

“Can this idea survive reality?”

Neither is sufficient alone.

In 2025 crypto markets — where volatility, narratives, and liquidity regimes shift rapidly — testing methodology matters more than strategy design.

Investors who treat testing as validation seek confidence.

Investors who treat testing as falsification build resilience.

That difference defines the gap between speculation and strategy.

Disclaimer

This article is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency markets are highly volatile and involve substantial risk. Past performance — whether from backtesting or forward testing — does not guarantee future results. Always conduct your own research and consider your risk tolerance before making investment decisions.

Rating of this post

Rate

If you enjoyed this article, please rate it.